Ever wonder how corporations track billions in revenue without losing a single cent? Financial clarity allows businesses to measure success, justify investments, and satisfy tax authorities. Without precise records, even massive enterprises would collapse under disorganized data.

In this blog, you will discover what accounting is and why every professional needs these skills. Readers shall explore fundamental categories, review practical scenarios, and understand core principles. This guide offers a clear roadmap through fiscal management techniques.

In this blog

What is Accounting?

Accounting is the systematic process of recording, categorizing, and communicating financial information regarding economic entities. Professionals capture every monetary transaction to create a clear history of business activity. This data helps stakeholders understand profitability, tax obligations, and remaining debt.

Retailers purchase inventory using credit while collecting cash from shoppers. Accounting tracks these transactions to show exactly how much stock exists and what bills remain due. Precise documentation prevents overspending while allowing owners to plan expansions based on actual cash flow. Consistent financial reports also prove business health to banks or investors. These documents show past growth and current asset values required for securing loans. Accurate records build trust with partners and provide a clear roadmap for future investments.

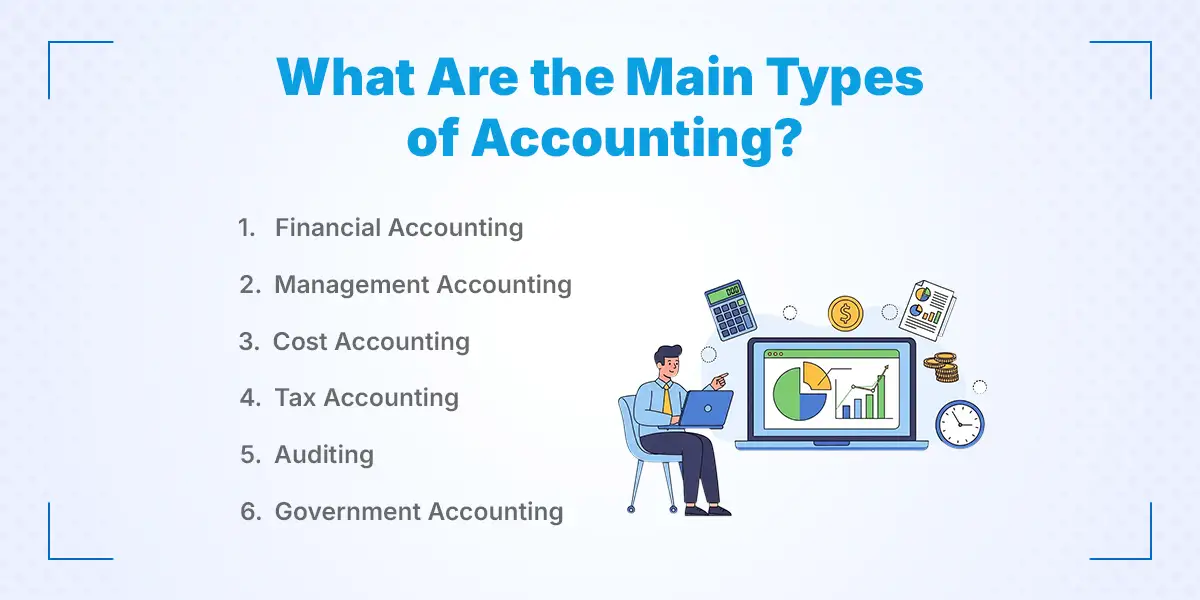

What Are the Main Types of Accounting?

The main types of accounting include financial, managerial, cost, tax, auditing, and governmental branches. Each discipline serves specific stakeholders by organizing fiscal data for different reporting goals. These categories ensure businesses meet legal requirements while providing leaders with tools for strategic planning. Organizations often combine several types to maintain complete oversight of monetary health and regulatory compliance.

1. Financial Accounting

Financial accounting involves preparing standardized statements for external parties such as investors, creditors, and regulatory agencies. Professionals follow established rules like Generally Accepted Accounting Principles to ensure consistency across different organizations. These reports, including balance sheets and income statements, reveal a company's overall performance during specific periods. Periodic audits confirm these summaries accurately reflect every transaction recorded during the fiscal year.

2. Management Accounting

Management accounting provides internal leaders with data needed for making informed operational decisions. Unlike public reports, these documents remain private and focus on specific departments or projects. Managers analyze current trends to forecast future needs, set budgets, and improve efficiency within the company. This branch prioritizes future growth strategies rather than historical reporting of past performance.

3. Cost Accounting

Cost accounting identifies every expense associated with producing goods or providing services. Experts examine variable costs like raw materials and fixed costs, such as factory rent, to determine price points for products. This analysis helps businesses eliminate waste and maximize profit margins on individual items. Detailed reports allow supervisors to pinpoint exactly where production bottlenecks increase overall manufacturing expenditures.

4. Tax Accounting

Tax accounting focuses solely on complying with internal revenue laws and government regulations. Specialists calculate taxable income, identify eligible deductions, and prepare annual filings to avoid legal penalties. This branch requires constant updates as tax codes change frequently at local and national levels. Proper tax planning helps organizations minimize liabilities while remaining fully compliant with state and federal requirements.

5. Auditing

Auditing provides an independent examination of financial records to verify accuracy and honesty. Internal auditors check for fraud or errors within their own company, while external auditors provide unbiased validation for shareholders. This process ensures that reported figures represent the true state of business affairs. Frequent reviews strengthen internal controls and prevent fiscal mismanagement or unauthorized spending.

6. Government Accounting

Government accounting tracks the allocation and usage of public funds by state or local agencies. This field emphasizes transparency and accountability to taxpayers rather than generating profit. Professionals ensure that departments stay within legislative budgets and use resources for intended social programs. Specialized tracking methods allow citizens to see exactly how tax contributions support infrastructure and public safety.

What Are the Key Functions of Accounting?

Key functions of accounting are recording transactions, classifying data, preparing reports, analyzing performance, and supporting strategic decisions. These core activities transform raw economic events into structured information for various users. By performing these tasks, departments ensure transparency, track resource movement, and maintain fiscal control. Organizations rely on these consistent steps to monitor liquidity and meet legal reporting obligations.

1. Recording Transactions

Recording involves identifying every economic event and entering details into a journal. Bookkeepers track sales, purchases, payroll, and loan payments as they occur to prevent data loss. This chronological log serves as the foundation for every other financial task within the firm. Precise entries ensure that no penny goes missing during busy operational periods.

2. Classifying and Summarizing Data

Classifying organizes recorded entries into specific groups like assets, liabilities, or expenses. Summarizing then condenses these numerous transactions into a ledger format for easier review. This process turns thousands of individual receipts into a clear overview of total spending and earnings. Systematic organization allows managers to view totals for specific categories without browsing every single receipt.

3. Preparing Financial Statements

Preparing statements involves creating formal documents like balance sheets, income statements, and cash flow reports. These papers communicate the economic status of a business to owners, banks, and government agencies. Standards ensure that anyone reading the reports understands the current wealth and debt levels of the entity. Standardized layouts provide a universal language for comparing different companies within the same industry.

4. Financial Analysis

Financial analysis uses past data to evaluate the strengths and weaknesses of an organization. Experts calculate ratios to determine if the business can pay short-term bills or if debt levels remain too high. This deep dive identifies trends that raw numbers might hide from a casual observer. Interpretation of these figures reveals whether the company is becoming more or less efficient over time.

5. Decision-Making Support

Decision-making support provides leaders with the evidence needed to choose future paths for the corporation. Accounting data helps determine if launching a new product line or closing a branch makes fiscal sense. By forecasting potential outcomes, professionals reduce the risk of costly mistakes in competitive markets. Reliable information ensures that growth strategies align with actual capital availability.

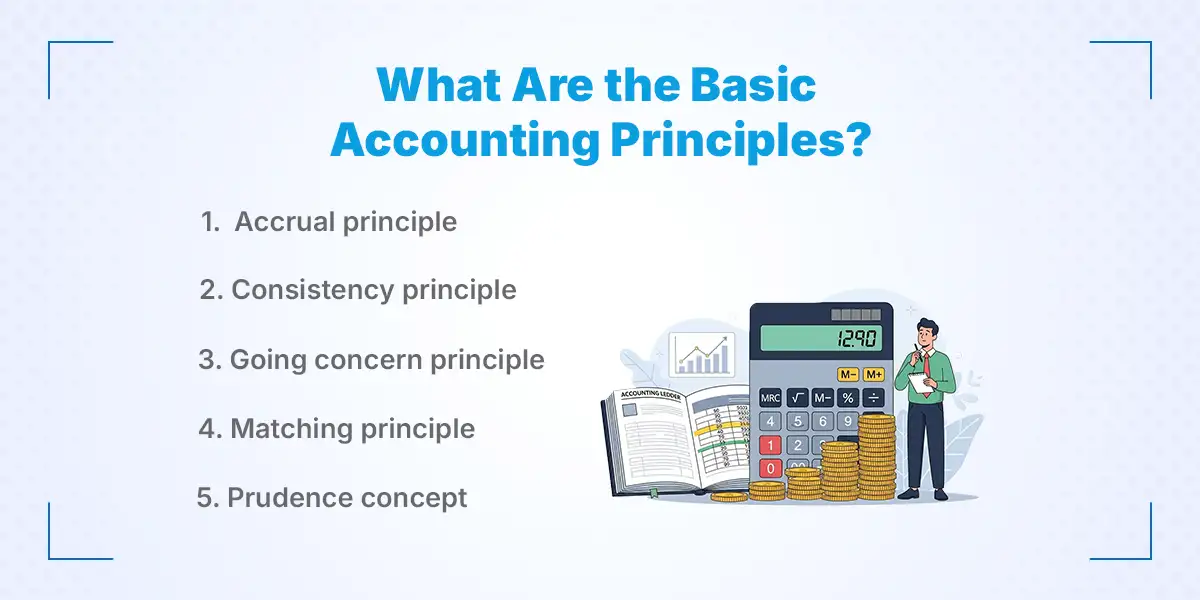

What are the Basic Accounting Principles?

The basic accounting principles are the accrual principle, the consistency principle, the going concern principle, the matching principle, and the prudence concept. These fundamental rules provide a standard framework for recording every financial event within a commercial entity. By following these guidelines, professionals ensure that statements remain transparent, reliable, and comparable across different industries. Consistent application of these norms prevents firms from hiding debts or inflating earnings to mislead stakeholders. Using these methods allows banks and investors to assess the true economic health of any organization accurately.

1. Accrual Principle

The accrual principle dictates that revenue and expenses are recorded when they occur, rather than when cash actually changes hands. For example, if a firm delivers goods in December but receives payment in January, the sale remains recorded in December’s books. This method provides a more accurate picture of current activity and future obligations. It prevents seasonal spikes in cash flow from distorting the actual performance of the business over time.

2. Consistency Principle

Consistency requires a company to use the same accounting methods and policies across different reporting periods. If a business chooses a specific way to calculate inventory value, it must stick to that method year after year. This allows external users to analyze trends and compare performance without being misled by changing calculation rules. If a change becomes necessary, the business must clearly disclose the reason and its impact on the reports.

3. Going Concern Principle

The going concern principle assumes that a business will continue to operate indefinitely into the foreseeable future. Because of this assumption, accountants can spread the cost of expensive equipment over many years rather than recording the full price immediately. It justifies carrying assets on the balance sheet at their original cost instead of their current liquidation value. Only when evidence suggests a company might fail do these valuation rules change to reflect a shutdown scenario.

4. Matching Principle

The matching principle ensures that every expense incurred to generate revenue is recorded in the same period as that revenue. If a car dealership pays commissions for sales made in June, those commission costs must appear on the June income statement. This prevents profit figures from looking artificially high in one month and low in the next due to timing gaps. Linking costs directly to the income they produce reveals the true profitability of specific business activities.

5. Prudence Concept

Prudence instructs accountants to choose the most cautious estimate when faced with uncertainty. This means recognizing potential losses immediately while only recording gains when they are certain to happen. For instance, if a customer might not pay a debt, a business records a "bad debt" provision in advance to avoid overstating its wealth. This principle protects investors by ensuring that financial reports do not paint an overly optimistic picture of assets.

What are Examples of Accounting in Real Life?

The examples of accounting in real life are salary and wage payments, business income and expenses, tax calculation, inventory records, and profit and loss calculation. These everyday activities involve tracking the flow of money to ensure financial stability and legal compliance. Individuals and businesses use these records to monitor spending habits and plan for future needs. Proper documentation allows for better resource management and prevents unexpected shortfalls. By organizing these figures, people gain a clear understanding of their economic standing.

1. Salary and Wage Payments

Employers must track hours worked by staff to ensure accurate compensation during each pay period. This process involves calculating gross earnings, subtracting insurance premiums, and withholding social security contributions. Accurate payroll records prevent disputes with workers and ensure the company remains compliant with labor laws. Maintaining these figures helps management understand the total cost of human labor for the organization.

2. Business Income and Expenses

Companies record every sale made to customers and every bill paid to suppliers to monitor cash movement. Tracking income reveals which products perform well, while monitoring expenses identifies areas where the firm might be overspending. This daily bookkeeping provides a live view of available funds for operations. Without these lists, a shop might run out of cash despite having high sales volume.

3. Tax Calculation

Accounting helps individuals and firms determine the exact amount owed to the government based on annual earnings. By listing all income and identifying legal deductions, taxpayers can reduce their total liability while staying within the law. Organized records make filing returns faster and provide evidence during potential audits. This systematic approach ensures that the entity contributes its fair share without overpaying.

4. Inventory Records

Retailers and manufacturers keep detailed logs of products currently held in storage or on shelves. These records track the cost of goods purchased versus items sold to prevent stockouts or excessive overstock. Knowing the value of physical inventory is essential for calculating the total assets of a business on a balance sheet. Regular updates help managers decide when to order fresh supplies from vendors.

5. Profit and Loss Calculation

At the end of a fiscal quarter or year, accountants subtract total expenses from total revenue to find the net result. A positive number indicates profit, while a negative figure shows a loss for that specific period. This calculation tells owners if their business model remains sustainable or requires immediate changes. These summaries serve as the primary report card for any commercial venture.

Why is Accounting Important for Businesses in Nepal?

Accounting is important for businesses in Nepal because it ensures legal compliance, fosters financial transparency, assists in strategic planning, and drives sustainable growth. In a landscape governed by the Income Tax Act and VAT regulations, precise record-keeping protects owners from heavy penalties. These systems provide a clear view of monetary health, allowing entrepreneurs to secure loans and attract investors. By maintaining accurate books, Nepali enterprises can navigate shifting market conditions while building a trustworthy reputation with government authorities.

1. Legal and Tax Compliance

Nepali businesses must adhere to strict regulations set by the Inland Revenue Department (IRD). Accounting helps firms calculate Value Added Tax (VAT) and Income Tax accurately to avoid legal disputes. Proper documentation ensures that companies meet annual audit requirements mandated by the Companies Act. Without these records, entities risk facing significant fines or suspension of their operational licenses.

2. Financial Transparency

Transparency builds trust between a business and its stakeholders, including employees, shareholders, and creditors. In Nepal, following the Nepal Financial Reporting Standards (NFRS) ensures that statements are honest and comparable to international benchmarks. Clear books prevent internal fraud and provide an unbiased look at how resources move through the organization. High transparency levels often lead to better credit terms with local banks.

3. Budgeting and Planning

Effective accounting allows managers to create realistic budgets based on historical earnings and spending patterns. In the fluctuating economy of Nepal, knowing exactly where money goes helps in prioritizing essential costs over unnecessary expenditures. Financial data serves as a guide for setting seasonal sales targets and managing cash flow during lean months. Planning with accurate numbers reduces the reliance on guesswork during major financial shifts.

4. Business Growth

Growth requires capital, and lenders in Nepal require proof of profitability before approving business loans. Accounting provides the necessary documentation to show a history of consistent revenue and asset management. Investors are more likely to fund projects that offer detailed financial projections and clear expense tracking. Systematic records allow owners to identify which products or services generate the most profit, enabling focused expansion.

Difference Between Accounting, Bookkeeping, and Auditing

Bookkeeping, accounting, and auditing represent distinct stages of financial management within a commercial entity. While bookkeeping involves daily data entry, accounting focuses on interpretation, and auditing provides final verification. Understanding these differences allows owners to assign the right tasks to specific professionals. Each process builds upon the previous one to ensure a complete and accurate history of monetary movements.

| Feature | Bookkeeping | Accounting | Auditing |

|---|---|---|---|

| Definition | Recording and organizing every daily transaction. | Summarizing and analyzing financial data. | Verifying and examining financial records. |

| Objective | Maintaining systematic logs of activities. | Determining profitability and performance. | Ensuring accuracy and legal compliance. |

| Timing | Continuous and ongoing daily tasks. | Periodic monthly or annual reviews. | Annual or specific project intervals. |

| Sequence | Begins when transactions take place. | Starts when bookkeeping tasks end. | Commences after accounts are final. |

| Focus | Clerical data entry and ledgers. | Analytical reports and statements. | Critical examination for errors. |

| Personnel | Performed by a bookkeeper. | Performed by a qualified accountant. | Performed by an independent auditor. |

| Deliverables | Updated journals and trial balances. | Balance sheets and tax returns. | Official audit reports and certificates. |

Career Scope of Accounting in Nepal

The scope of accounting is increasing in Nepal as every business sector requires financial expertise for daily operations and legal compliance. Professionals find stable employment in diverse fields ranging from local startups to international organizations. Demand remains high as the economy grows and government tax regulations become more rigorous. Skilled accountants enjoy competitive salaries, long-term job security, and clear pathways to executive leadership roles. Using modern software like Tally or Excel further enhances employability in this evolving market.

1. Jobs in Private Companies

Private firms represent the largest employers for accounting graduates in Nepal. Small businesses hire accountants to handle daily bookkeeping, payroll, and VAT filings. Large corporate houses offer specialized roles in financial planning, cost control, and internal reporting. These positions allow professionals to gain versatile experience across different business functions.

2. Banks and Financial Institutions

Commercial banks and insurance companies hire accountants for treasury management, risk assessment, and compliance roles. These institutions offer structured career paths with higher starting salaries and performance-based bonuses. Professionals in this sector ensure that all transactions meet the strict guidelines set by Nepal Rastra Bank. Structured environments provide excellent opportunities for those interested in financial strategy and corporate finance.

3. Audit Firms

Working in audit firms involves verifying financial statements and ensuring clients follow national accounting standards. Junior auditors gain exposure to multiple industries, which builds technical expertise quickly. These firms often serve as a training ground for those pursuing professional certifications like CA or ACCA. Experts in this field help businesses maintain transparency and prepare for annual tax assessments.

4. NGOs and INGOs

Non-governmental and international organizations require accountants to manage donor funds and project-based budgets. Professionals in this sector focus on grant reporting, transparency, and strict adherence to donor guidelines. These roles often offer attractive benefits and the chance to work on social development projects across various districts. Expertise in fund accounting is highly valued by international partners operating within the country.

5. Career Growth Opportunities

The accounting field offers a clear ladder from entry-level assistant to senior management positions like Finance Manager or CFO. Earning professional degrees such as Chartered Accountancy (CA) significantly boosts earning potential and authority. Continuous learning through workshops on new tax laws or digital tools ensures long-term relevance in the job market. Experienced professionals can also establish their own consultancy firms to provide freelance tax and advisory services.

Which Is the Best Accounting Training Institute in Nepal?

Kumari Job is the best accounting training institute in Nepal because it offers a highly practical, job-oriented curriculum designed by industry experts. Their program stands out by bridging the gap between university theories and real-world workplace demands in the Nepali context. Students benefit from hands-on training in taxation, VAT, and popular software, ensuring they are ready for immediate employment. Additionally, the institute’s strong ties to a vast network of employers provide graduates with unmatched job placement support and internship opportunities.

1. Factors to Consider When Choosing an Accounting Training Institute

Selecting the best accounting training services requires evaluating several critical factors to ensure a high return on your investment. You should prioritize centers that offer a curriculum updated with the latest Nepal Financial Reporting Standards (NFRS) and current tax laws. It is also essential to check for a proven track record of student placements and positive alumni reviews within the Nepali job market. Location, affordable fee structures, and the availability of flexible class timings for working professionals are also key practical considerations. Finally, ensure the institute provides a recognized certificate that adds genuine value to your professional resume.

2. Importance of Practical Training, Software Skills, and Experienced Trainers

Theory alone is insufficient for success in a modern finance department; therefore, practical training is the most vital component of any course. Mastering software like Tally Prime and Advanced Excel allows you to process transactions and generate reports with speed and accuracy. Learning from trainers who have years of experience in audit firms or corporate houses ensures you receive "insider" tips that textbooks cannot provide. This combination of hands-on practice and expert mentorship builds the confidence needed to handle complex tax filings and financial audits. Modern employers actively seek candidates who can demonstrate these technical skills during the interview process.

Conclusion

Accounting serves as the language for every business, transforming raw numbers into meaningful stories regarding financial health. By mastering these vital skills, individuals and companies gain the power to make informed decisions while maintaining strict legal compliance. Organizations prioritizing accurate record-keeping find themselves better positioned to navigate market shifts and secure long-term stability.

Learning these principles provides a significant advantage for career growth. For entrepreneurs, these skills are essential for managing daily cash flow and proving company value to potential investors. Mastering modern digital tools and staying updated on local tax regulations ensures you remain a vital asset in the competitive Nepali job market. Investing time in this knowledge builds a strong foundation for achieving lasting professional goals.

Frequently Asked Questions

Submit your comments

Get Our App On

How to Make a Police Report (Police Clearance Certificate) in Nepal?

VIEW DETAILS

Types of SEO and How They Work: Complete Beginner's Guide

VIEW DETAILS

Government Restricts New Lok Sewa Vacancy Requests 2083/84 — Or Not?

VIEW DETAILS

How to Apply for Tattoo Artist Jobs in Nepal?

VIEW DETAILS

Loading Comments...